The Netflix quarterly earnings update is an exciting time for members of the Blue Chip team. In its opinion, Netflix has an enviable culture and is led by a visionary (and highly credible) management team who think deeply about the future of content consumption and how they can continuously innovate to increase engagement levels with their consumers. Listening carefully to teams who possess such characteristics can give one important insights about the long-term direction of travel and this often provides us with the confidence to forgo the consensus narrative in favour of a dose of independent thinking.

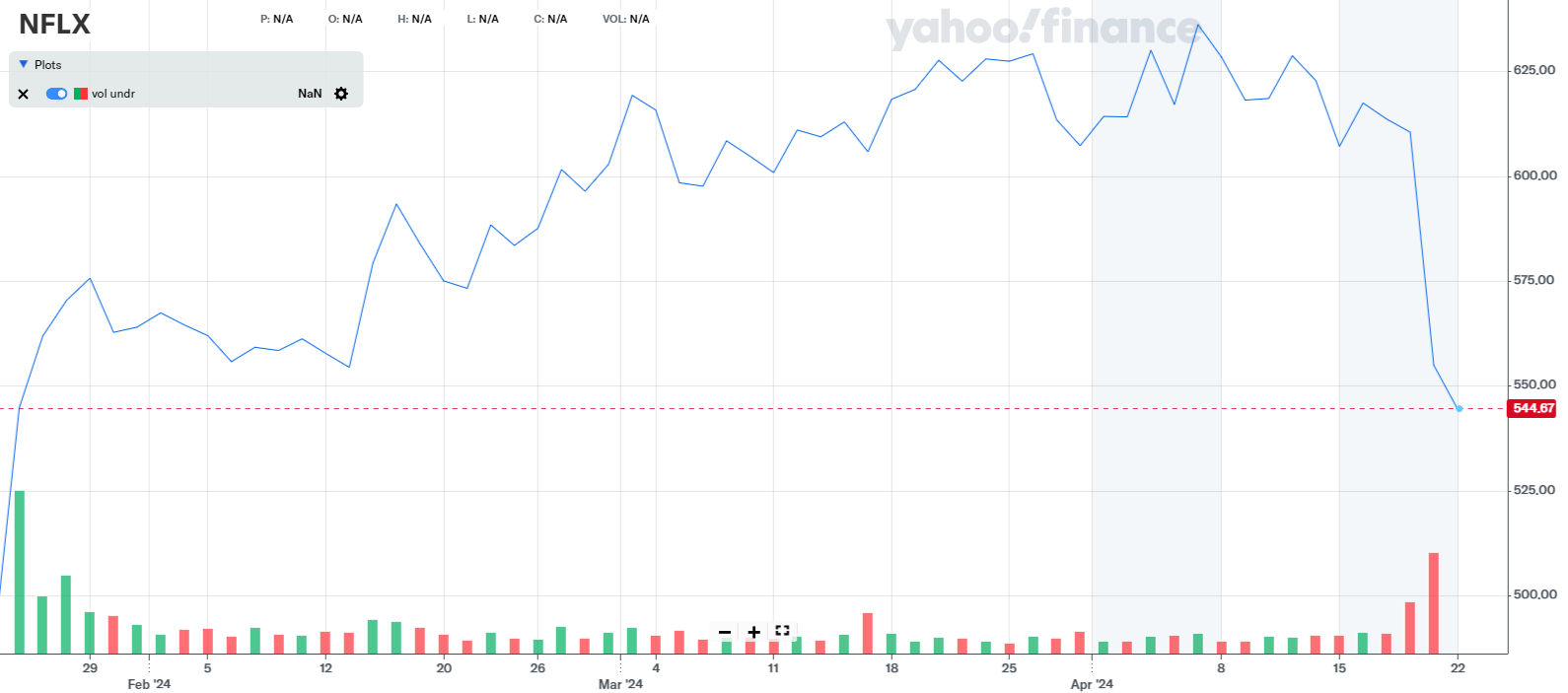

Last Thursday, Netflix provided investors with an update on its performance for the first quarter of its fiscal year. Paid subscriber growth was up 16%, revenues were up 15%, operating income increased 54%, operating margins increased 700 basis points to 28% and management even raised their guidance for the full year to reflect the strong start. After such a solid set of results, you’d be forgiven for assuming that Netflix shares would have reacted favourably. The reality was a little different – the shares declined roughly 10%.

So, what had the company done to upset the analytical community? As part of the announcement, management prewarned analysts that, from 2025, they would cease providing quarterly subscriber numbers given the decreasing relevance as a metric to assess the company’s overall performance. In the past, company revenues were a product of subscription price and the number of members. Today, with the growing number of revenue streams (including advertising), localised pricing strategies and various subscription tiers the basic equation no longer holds true. Netflix now has revenue levers beyond simply adding subscribers which, for the rational investor, should be a pleasing development.

The negative response is a perfect illustration of the precision fallacy (we discuss this further in our upcoming Blue Chip Quarterly Insights, so keep an eye out on our website for that) and the shortcomings associated with relying on valuation models driven by very specific inputs. Netflix’s decision to change the metrics it discloses has essentially rendered these models useless and stumped analysts who, heaven forbid, will now have to come up with new methods (no doubt equally as complicated) of determining Netflix’s value.

Luckily, our investment process does not depend on such pernickety models. Instead, we’ve been focusing on what management had to say and the progress the company is making on its strategic developments. With all the noise surrounding the disclosure announcement, here’s a few things you may have missed:

- “A good general guideline for us in the long-term is that it would be healthy for us to land overall monetization between our ads and non-ads offerings at roughly an equivalent position.” In other words, from a financial perspective, management are aiming to get to the position where they are agnostic on whether a subscriber or advertising-led model triumphs.

- “We looked at the population non-impacted by paid sharing. The hours viewed per account were steady with the year ago quarter.” Engagement levels are holding up well if you exclude the short-term impact from the removal of customers who were previously using someone else’s account to artificially inflate viewing hours.

- “As we add more entertainment value, then of course we can go back to our subscribers and ask them to pay a little bit more to keep that virtuous cycle moving.” This is exactly the type of pricing strategy we like to see. Focus on delivering value for your customers, increase their willingness-to-pay and then, only after this, do you consider increasing prices (please see our 2023 Q2 newsletter which discusses the value stick framework in more detail).

We continue to believe Netflix is executing well and that management remain laser focused on the factors important for long-term success.